Shared ownership is a scheme run by the government that allows first-time buyers to get a foot on the property ladder. Instead of buying the full property, you are able to buy a share of a property, allowing you to take out a smaller mortgage and put down a smaller deposit.

You can increase the share that you own further down the line by following a process called ‘staircasing’ and can eventually own 100% of the property.

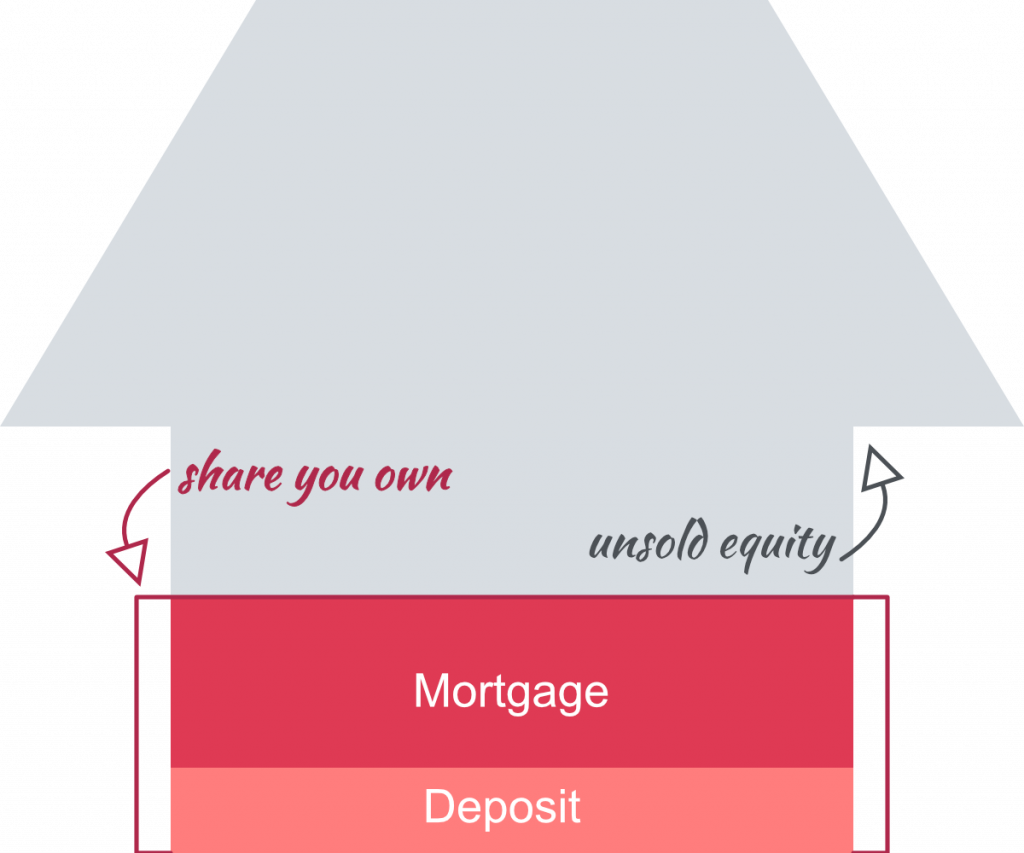

Shared ownership is an affordable homeownership scheme where instead of putting a deposit down and taking out a mortgage for a full property, you buy a share of it, usually somewhere between 10% and 70%. For the remainder of the property, known as unsold equity, you pay subsidised rent. This does not apply to all houses; properties must have been built for that scheme by a housing association using government subsidy.

What's Included?

How much are my monthly payments?

This can seem confusing, as you have both rent and mortgage payment each month. Don’t fret though – both of these are subsidised to reflect the amount of the share that they cover. The rent works out cheaper than you’d generally find as well, so you could find yourself spending less monthly than you did when you were renting.

So, you would pay a mortgage amount on the share, e.g. 10%, and pay rent on the other 90% (that is unsold equity). As you are only buying a share of the property, the deposit required is significantly reduced as you only need from 5% of the share you are purchasing.

Why choose shared ownership?

A lot of first-time buyers choose shared ownership as the regular method of buying a home and the large deposit it required was not affordable for them. Shared ownership cost significantly less as you need a much smaller deposit, the rent tends to be cheaper than on the open market, and stamp duty can be deferred until you own 80% or more of the property.

You’re not tied in to only owning that share for life either – later down the line you can buy more, depending on what you can afford and eventually own the entire property.

Am I eligible for shared ownership?

You do have to fit into the eligibility criteria in order to be considered for shared ownership, these are:

- You must be 18 or over

- Your income must be less than £80,000 annually (£90,000 in London).

- You should be a first-time buyer

- You should not be able to afford a home on the open market that is suitable for you

- You should not have any mortgage or rent arrears

- You need a good credit history

- You can boost your creditworthiness with credibble.com for free! Sign up here.

- You must be able to afford the regular payments and costs involved in buying a home.

- You should have savings of around £4000 to cover the costs

- These costs vary, but this is the ballpark figure they tend to suggest.

- You need around 5-10% of the share you plan to buy as a deposit.

- You can go as low as 5%, but mortgage rates tend to get better at 10%.

Who is prioritised in shared ownership?

Shared Ownership is available to anyone, regardless of your age, so long as you are eligible. Because of this, some people may be prioritised over others such as:

- Military members.

- In some cases, priority may be given to those who live and work in the area already, this is put in place by the local council.

- If you own a home already then you must show that you are in the process of selling it.

What happens with maintenance and repairs in shared ownership?

If you currently rent, then you’re likely to be aware that costs of maintenance costs and repairs generally fall to your landlord or landlady, so it’s easy to think that these costs would be split, however, this is not the case. Regardless of how much of the home you own, all repairs and maintenance are your own responsibility. If it is a new build, then there is usually a one-year warranty to cover any defects.

If you’re purchasing a flat then you’ll probably have to pay some kind of service costs which will cover repairs, maintenance, and cleaning of any communal areas such as stairways and lifts.

Staircasing

Despite the name, this has nothing to do with the stairs in the property and actually refers to the process of owning more of the property than you started with.

When you buy a home with shared ownership, you start off with somewhere between 10% and 75% of your property depending on what is available and affordable for you. This will also depend on whether it is a resale property, as the minimum will be the same or more than the seller previously owned.

You should then be able to staircase (i.e. own more) in 10% increments – the cost of this will be determined by the value of the property when you choose to staircase. Normally, you’ll be able to do this as and when you can afford to do so.

You can staircase all the way to 100%, however, in some cases, there is a cap on how much of the property you own. Of course, as you own more of the property your rent payments will decrease and your mortgage payments will increase. Eventually, you will not pay any rent and only the mortgage payments.

Other costs?

While shared ownership does significantly reduce the upfront costs of purchasing a home, it doesn’t remove any of the extra costs that come with buying a home. You still need to pay solicitor fees, moving costs and survey fees. The only cost which will differ will be stamp duty.

You will get the option on whether or not you want to pay the stamp duty on the full cost of the property, not just the amount you are buying. This means that if you go on to own more of the home, you will not have to pay stamp duty again. Of course, this is an upfront cost, so you’ll need to have some disposable cash to use on this.

The alternative is to pay stamp duty on the amount you are buying only – this may result in you paying more stamp duty overall, but it will reduce the initial costs. Your solicitor or legal advisor will be able to give you more information on how much you will be liable to pay and when no matter which one of the above you choose to do.

Mortgage

You will make payments on your mortgage every month until it is fully paid, this will be on the remainder of your share after your deposit. If you choose to purchase more of the property, you are able to extend your mortgage for this, however, this will depend on the mortgage provider and the terms of your agreement.

The amount you pay monthly on your mortgage will be determined by your mortgage provider and may be a percentage or a fixed amount.

Rent

Your rent will usually be around 3% of the unsold equity. You can work this out below:

Value of property* share you don’t own = unsold equity

Unsold equity*0.03= Rent payable annually

Annual rent /12 = Monthly payment

If you’d like to take a look at other affordable homeownership schemes, then you can also read our articles on Help to Buy ISAs and Help to Buy equity loans.

Credibble offers two fabulous solutions

If you’re preparing to take a mortgage, never apply until you’ve tried our unique and FREE Credibble Home app. Our smart technology will tell you what you need to fix so you avoid rejection. The app predicts when you will be able to buy, for how much and tracks your month-by-month progress to mortgage success. We’ve even added your own mortgage broker, so you get the best deals available.

More focused on your credit rating? Well, get started for free with Credibble’s 24- Factor Credit Check to truly help you improve your creditworthiness and how lenders view you. (Remember: lenders don’t use your credit score! We’ll show you what lenders look for and how to get your credit report in the best shape possible).

Last updated by Robert Edwards, July 2022