One of the six Credit Factors on Credibble’s 24-Factor Credit Check is based on your stability. Good credit isn’t just about responsible borrowing and attention to your financial health. It’s also about who you are as a person. Lenders want to see you as an established person with reasonable status.

What's Included?

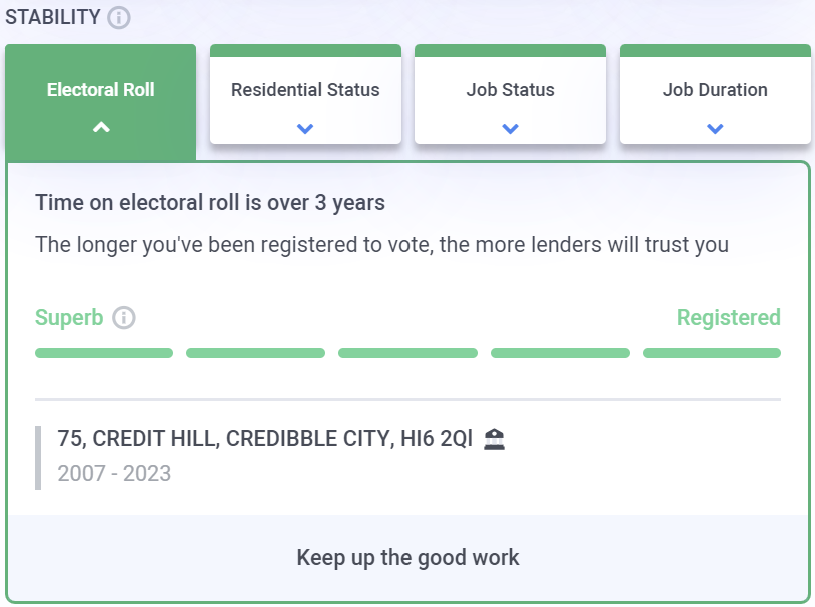

Electoral Roll

A great way of confirming your identity is by registering to vote. This means your name and other personal details, like your address, will show up on the electoral roll. Lenders can access this information and use it for the purpose of confirming that you are who you say you are. This saves a few headaches for you and the lender.

Some people avoid getting on the electoral roll because they don’t wish to vote. Alternatively, they don’t want to go on the Open Register, which is a version of the electoral roll available for commercial use.

Our take at Credibble is this: The UK is a parliamentary democracy. You are not obligated to vote if you don’t want to. Democracy means having the right to abstain from voting as much as it means having the right to vote. Being registered to vote doesn’t mean the Government can make you vote.

What’s more, lenders don’t use the Open Register to verify your information. Therefore, you don’t even have to go on the Open Register to count. It’s a no-brainer, really.

Bear in mind that registering to vote is available to British, Commonwealth, Irish and EU citizens. EU citizens generally can’t vote in UK parliamentary elections, but Cypriots and Maltese resident in the UK can. Citizens of the United States of America may not register to vote.

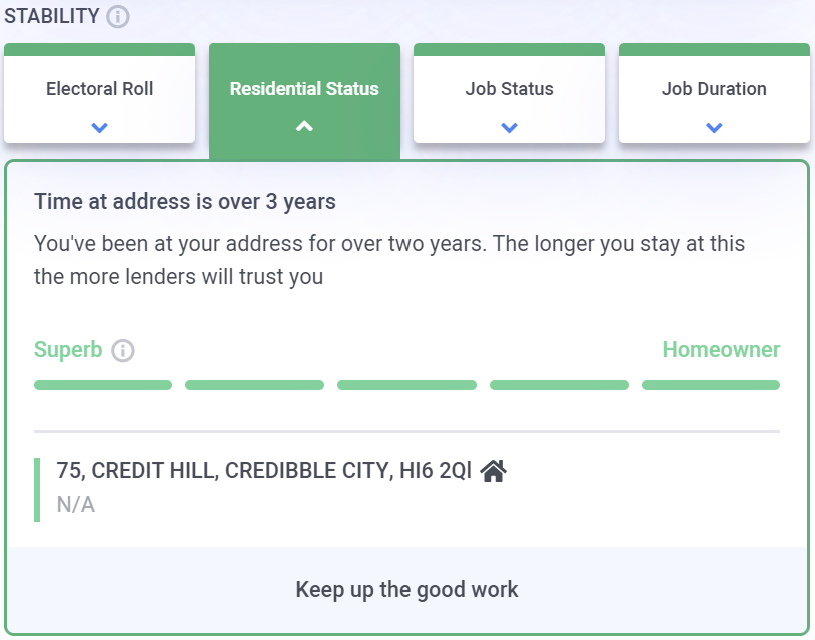

Residential Status

Lenders want to see that you’ve been living at the same fixed address for two years. Whether you live with parents or rent a place, lenders want to know that you have some stability. If you are constantly moving from place to place, that might indicate problems paying rent or other financial troubles.

The best residential status to have in the eyes of lenders is to be a homeowner. This indicates you have firmly put roots down and won’t be going anywhere any time soon.

The longer you stay in one place, the better trust lenders will place in you.

- ⭐ Our 24-Factor Credit Check goes beyond your credit score.

- ⭐ See your credit report through a lender’s eyes.

- ⭐ Personalised steps to improve your credit rating.

See… Fix… Borrow… with Credibble.

START FREE TRIALJob Status

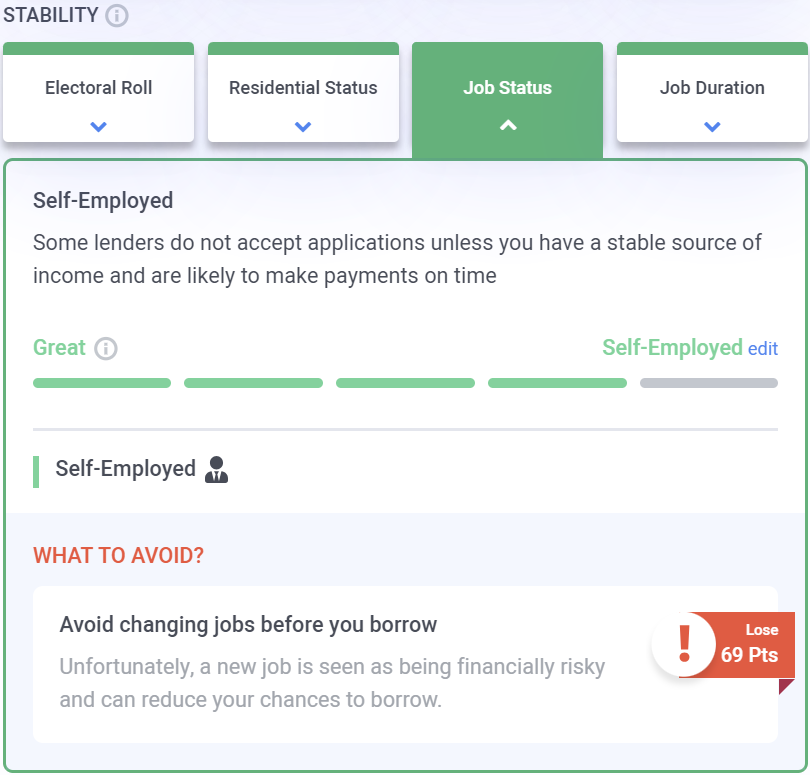

Employment means income, so if you’re employed, that’s a good sign to lenders that you will be able to make payments. Full-time employment with a decent is ideal, though even part-time employment can improve your credit score. Remain in your job for multiple years, and it can boost your score even more!

Job Duration

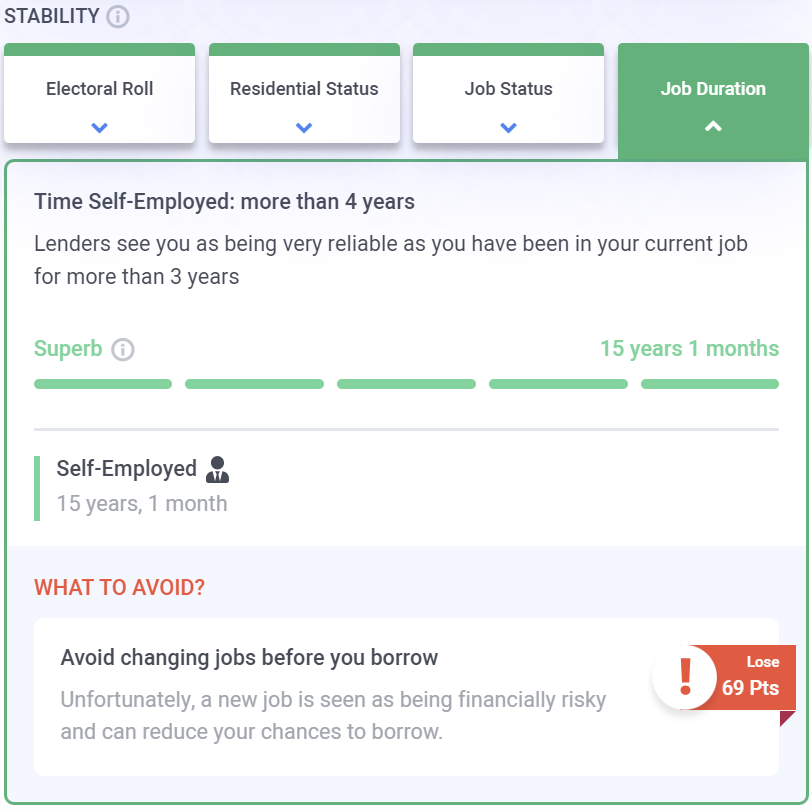

Lenders have more confidence in borrowers who have been in their current job for more than twelve months. After twelve months, workers generally have enough experience and are settled in enough that they’re not likely to be moving along any time soon.

The longer you stay at a job, the better you’ll look to lenders.

Credibble offers two fabulous solutions

If you’re preparing to take a mortgage, never apply until you’ve tried our unique and FREE Credibble Home app. Our smart technology will tell you what you need to fix so you avoid rejection. The app predicts when you will be able to buy, for how much and tracks your month-by-month progress to mortgage success. We’ve even added your own mortgage broker, so you get the best deals available.

More focused on your credit rating? Well, get started for free with Credibble’s 24- Factor Credit Check to truly help you improve your creditworthiness and how lenders view you. (Remember: lenders don’t use your credit score! We’ll show you what lenders look for and how to get your credit report in the best shape possible).