One of the six Credit Factors on Credibble’s 24-Factor Credit Check is based on whether you have bad credit. These factors are very important, as they indicate to lenders that your reputation is in good standing. Having bad credit can seriously impact your access to credit. You may not be able to borrow as much or at all, or you may face higher interest rates.

What's Included?

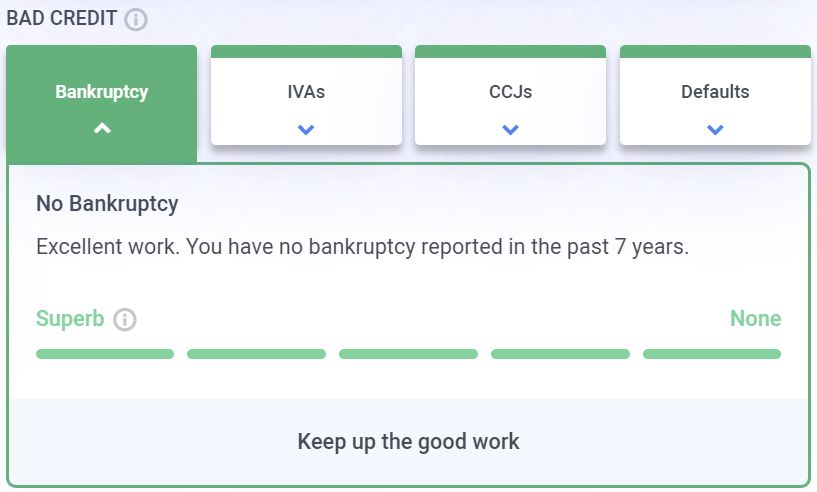

Bankruptcy

In UK law, you can apply to become bankrupt if you cannot pay off your debts. This is usually the last-resort “nuclear option”.

When you have tried everything else to pay off your debts, or a licensed financial advisor has advised you to do so, you may declare bankruptcy. You can also be made bankrupt if you fail to pay debts of £5,000 and up, you break the terms of an IVA (see below), or you give false information to an IVA.

For most people, bankruptcy isn’t likely to be a concern, but careless borrowing can result in bankruptcy. Small business owners, particularly in volatile industries like the catering industry, are more likely to suffer a bankruptcy. However, it can happen to anyone. In March 2022, there were 633 bankruptcies in England and Wales, down from 1,028 the previous March.

If you have had a bankruptcy in the last seven years, it will negatively affect your credit score. After that time has passed, it’s striped from the record.

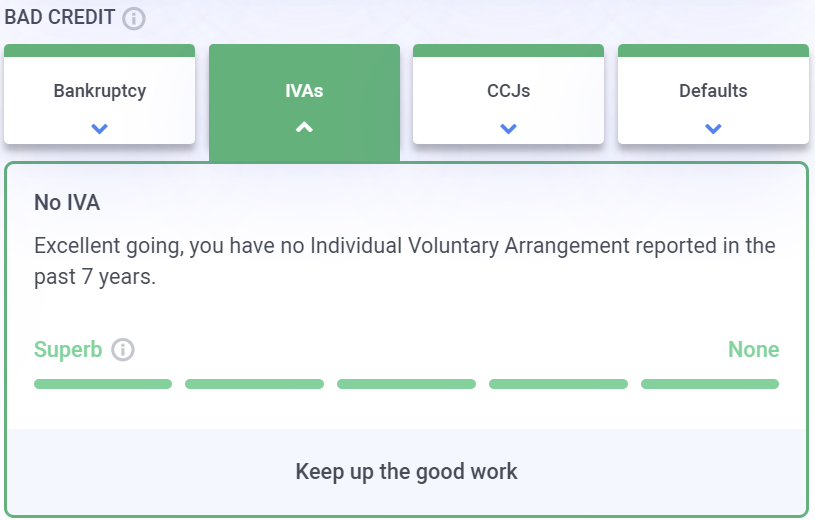

IVAs

IVA stands for “Individual Voluntary Arrangement”. It’s an alternative to bankruptcy for people living in England and Wales. If your debts become too much to manage and you enter insolvency, you can contact a professional insolvency practitioner to set one up. In practice, an IVA is a legal agreement between you and any parties to whom you owe money. Both sides agree on a repayment plan, and both have to stick to it. Any income you receive, including windfalls, will be used to pay off the IVA.

IVAs negatively affect your credit rating. They show that your debts have gone so out of control that you’ve had to call in outside help. Like bankruptcies, these remain on your credit file for seven years, after which they are striped from the public record.

If you lie on an IVA, or you break the legally-binding terms, you can be made bankrupt by creditors. This will have an even worse effect on your credit rating.

- ⭐ Our 24-Factor Credit Check goes beyond your credit score.

- ⭐ See your credit report through a lender’s eyes.

- ⭐ Personalised steps to improve your credit rating.

See… Fix… Borrow… with Credibble.

START FREE TRIALCCJs

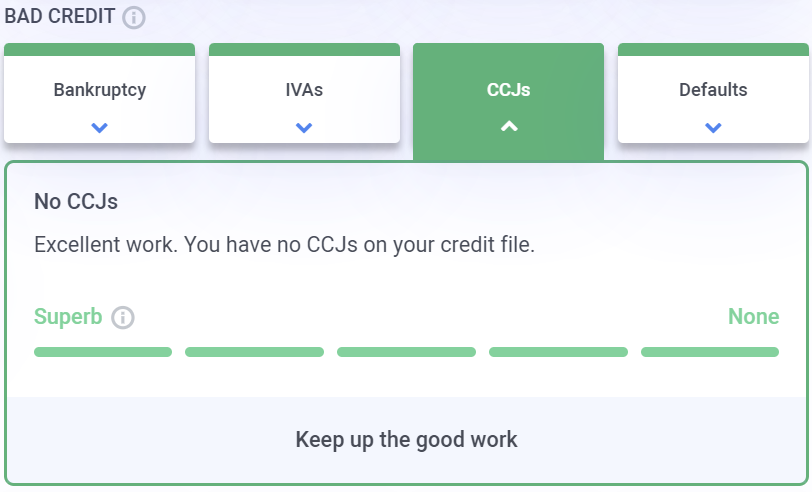

A CCJ is a County Court Judgement. Like IVAs, they only take place in England and Wales. They are handed down by the court in response to a court action against you made by a creditor. Usually, this is because you owe a sum of money. You will be sent a letter fourteen days in advance of the judgement, giving you time to respond to the allegation.

If you fail to respond adequately, the court may secure your debt against property. This permits your creditors to demand direct payment from your employer or your bank. In extreme cases, the County Court can send in bailiffs to seize goods and auction them off.

CCJs lower your credit score because they once again show that you have failed to keep on top of your debts, requiring a legal response. CCJs are removed from your credit file after six years.

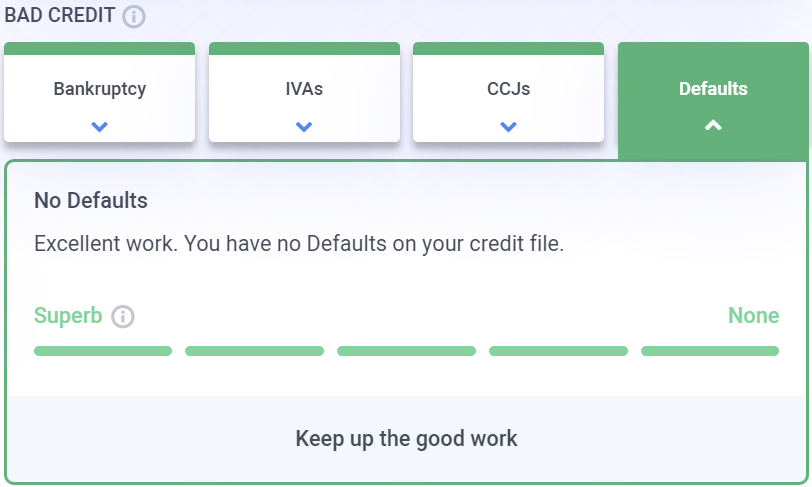

Defaults

If you fail to pay your debts, a creditor may close your account. This is what is known as a “default”. You can default when you owe any amount of money. You may think that this is less severe than a bankruptcy, an IVA or a CCJ, but bad credit is bad credit, any way you slice it.

Like other bad credit, defaults don’t leave your credit file for at least six years. However, it is possible to lessen the impact of a default. Pay off the debts in a timely fashion. You can also ask one of the three Credit Reference Agencies to append a statement of explanation to your report if the default. was down to circumstances beyond your control.

All of these things will go away with time – between seven and ten years. They aren’t a death sentence, but bear in mind that they are likely to cause trouble getting the best deals on credit. The good news is that proving yourself creditworthy through responsible borrowing can lessen the impact of even the worst credit, given enough time. Just be aware you may not have access to the nicest deals.

Credibble offers two fabulous solutions.

If you’re preparing to take a mortgage, never apply until you’ve tried our unique and FREE Credibble Home app. Our smart technology will tell you what you need to fix so you avoid rejection. The app predicts when you will be able to buy, for how much and tracks your month-by-month progress to mortgage success. We’ve even added your own mortgage broker, so you get the best deals available.

More focused on your credit rating? Well, get started for free with Credibble’s 24- Factor Credit Check to truly help you improve your creditworthiness and how lenders view you. (Remember: lenders don’t use your credit score! We’ll show you what lenders look for and how to get your credit report in the best shape possible).