One of the six Credit Factors on Credibble’s 24-Factor Credit Check is based on your use of short-term credit. Some short-term credit looks good on your credit report. Some doesn’t. In this article, we’ll be talking about the dos and don’ts of short-term credit.

What's Included?

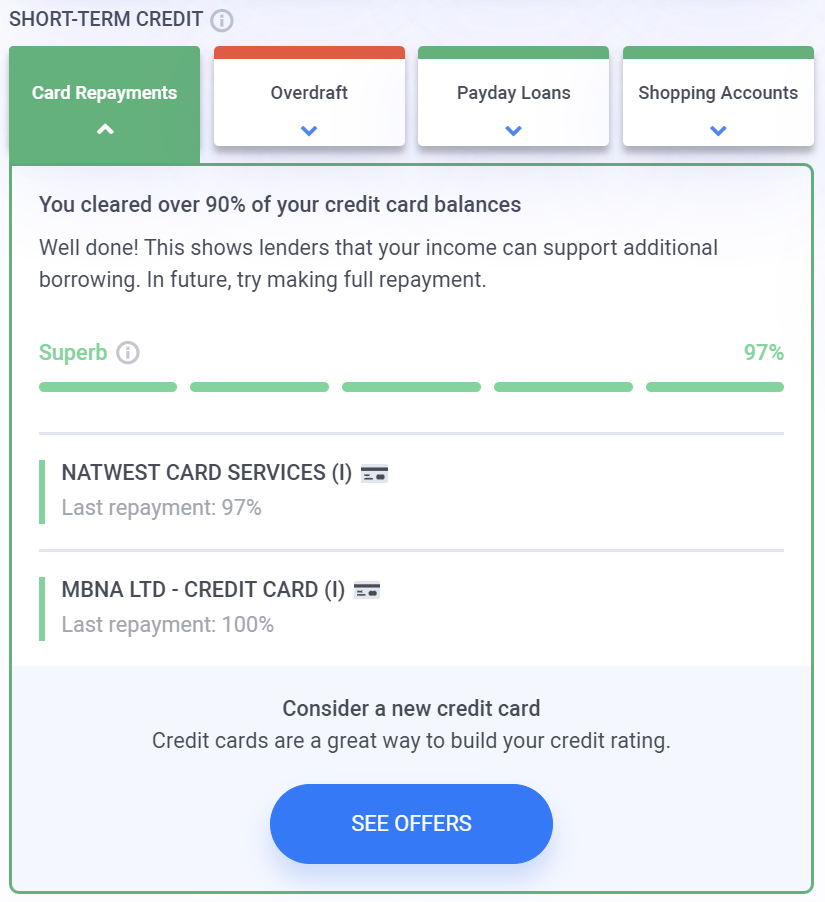

Card Repayments

In another article, we talked about how credit cards can be useful for building credit. Having and using one can be good, of course, but you also have to pay the money back! The name of the game here is keeping on top of credit card debt. Aim to pay off the total balance every month, not just the minimum payment the card issuer requires you to pay. This is easier, of course, if you’re only aiming to use less than 30% of your limit.

Credit card issuers will often let you keep paying the minimum for months and months, but remember that interest will start to accrue (even if you have an interest-free offer – remember, it will end sooner than you think). So it’s no skin off their nose if you don’t pay off the balance – it just means more money for them!

Lenders might see you failing to pay off your balance as a sign of irresponsibility. It suggests someone who borrows money but isn’t reliable when it comes to repayments. So making repayments in full and on time is a great way to show you have good habits.

Overdraft

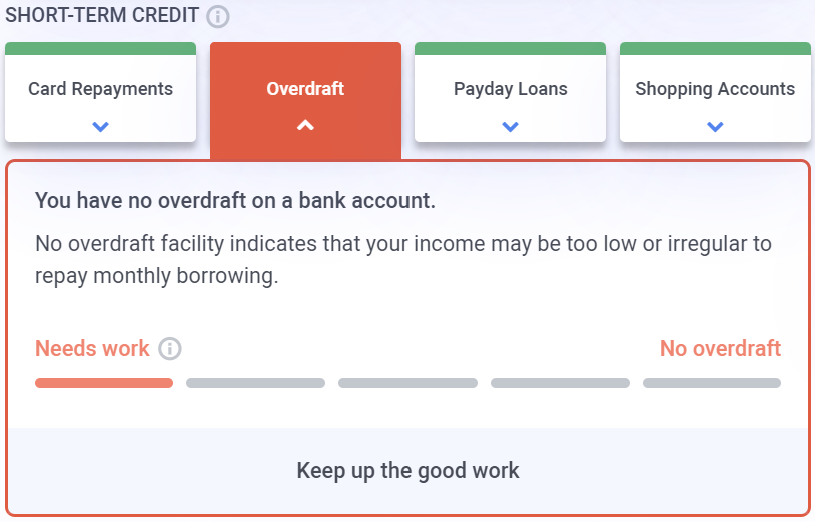

Arranging an overdraft on your current account is similar to having a credit card, but with some key differences. For starters, withdrawing from an account with an overdraft doesn’t affect your credit score in the same way that withdrawing on a credit card does.

Because an overdraft is attached to your account and your money, credit agencies don’t generally have access to detailed information. This is for privacy and security reasons. It’s simply whether or not you have an overdraft.

Not having an overdraft sends the message that your income is too low or irregular to repay. It can be good to have one, even if you have enough cash in your account to never feel a need to tap into it.

Just remember that an overdraft is a form of credit, so it does charge interest, often at a higher rate than credit cards. It does not, however, have a minimum repayment. However, the institution with which you hold the account can usually demand partial or full repayment at any time.

- ⭐ Our 24-Factor Credit Check goes beyond your credit score.

- ⭐ See your credit report through a lender’s eyes.

- ⭐ Personalised steps to improve your credit rating.

See… Fix… Borrow… with Credibble.

START FREE TRIALPayday Loans

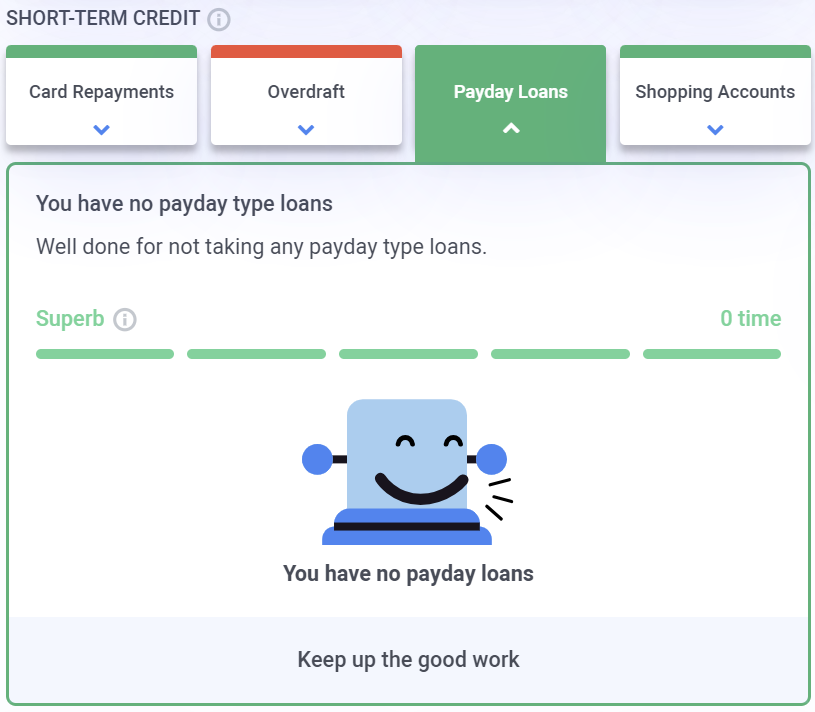

Let’s cut right to the chase: Payday loans are usually a bad deal.

They’re short-term but extremely high-interest. Many payday loans have APRs in excess of 1,000%! To put that in context, most credit cards have APRs under 50%.

Bear in mind, however, that this is mostly meaningless since payday loans aren’t meant to be paid off over years, just weeks or months.

Still, this should clue you in to the fact that even payday lenders who do everything above-board and in accordance with FCA regulations can be offering a bad deal to borrowers.

While there are certain limitations to the amount lenders can charge you in a short timeframe, these loans are still bad for your credit report.

When a lender sees you have applied for a payday loan, it sends the message you are desperate for money. Much like withdrawing cash on a credit card, it indicates that you can’t live on your income alone.

Before applying for a payday loan, we suggest that you seek out alternative solutions first.

Shopping Accounts

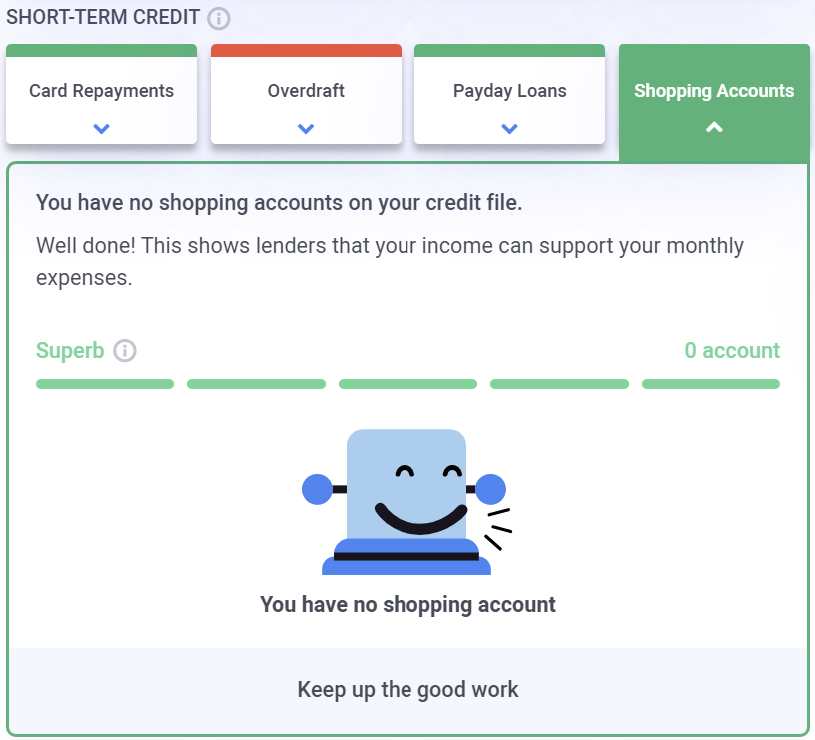

You’re shopping for a new outfit on a clothing website, and go to the payment screen. Once there, the checkout offers you a choice: Pay the balance in full now, or pay the balance in instalments over a set period of time. Wow, you might think. I can wear this outfit to next week’s party and not have to worry about paying for drinks!

These “buy now, pay later” offers may be tempting, but racking up too many of them can cause problems. They are a form of short-term credit known as “shopping accounts”, even if they don’t seem that way.

It’s perfectly normal in some cases to pay for items in instalments. Appliances and furniture are often sold this way, so you don’t have to spend thousands in one go. However, these repayments often take place over a much longer period of time, meaning they’re more like proper loans.

As with many things, a “buy now, pay later” once in a while may not do much harm, but doing it repeatedly, for every new outfit you buy? That’s when lenders will start to get leery. Once again, it makes you look strapped for cash, and lenders simply can’t afford to take the risk.

So, be cautious, and consider whether you can afford to pay for that outfit in full. Plus, do you really need those extra drinks? Your credit score, and your liver, will thank you to be a bit more wary!

Credibble offers two fabulous solutions

If you’re preparing to take a mortgage, never apply until you’ve tried our unique and FREE Credibble Home app. Our smart technology will tell you what you need to fix so you avoid rejection. The app predicts when you will be able to buy, for how much and tracks your month-by-month progress to mortgage success. We’ve even added your own mortgage broker, so you get the best deals available.

More focused on your credit rating? Well, get started for free with Credibble’s 24- Factor Credit Check to truly help you improve your creditworthiness and how lenders view you. (Remember: lenders don’t use your credit score! We’ll show you what lenders look for and how to get your credit report in the best shape possible).