One of the six Credit Factors on Credibble’s 24-Factor Credit Check is based on your payment history. We look at your payment history over 24 months and see if you’ve been up to date on repayments with any loans you may have. As a way of determining creditworthiness, lenders are interested in this, because it shows your reliability as a borrower.

What's Included?

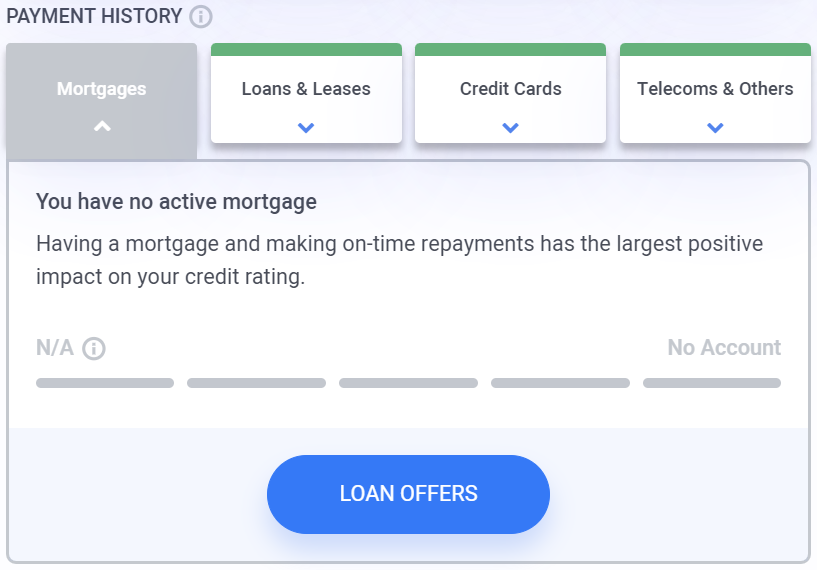

Mortgages

The good news: Having a mortgage and keeping up with repayments on it is the single best thing you can do for your credit rating. The bad news: You need a good credit rating to get a mortgage. The only way to get a good credit rating is to have a good credit history.

Hmm.

Not to worry – if you’re looking to improve your credit rating before applying for a mortgage, and you don’t have a mortgage, this isn’t a mark against you. It just means you need to look elsewhere to start building a credit reputation.

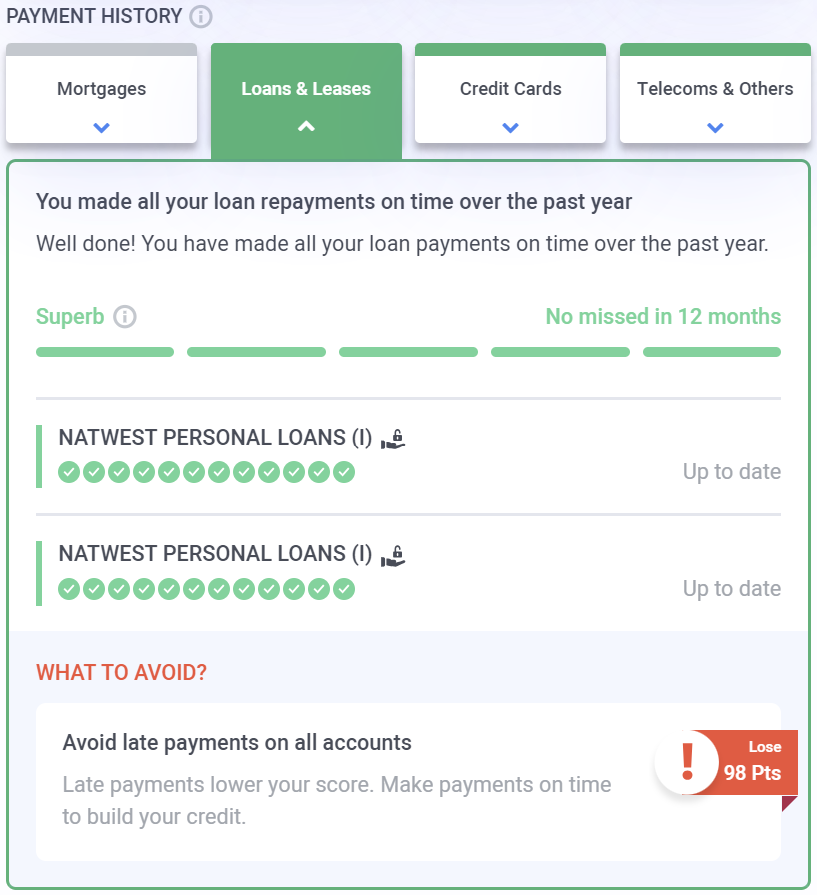

Loans & Leases

Having a smaller loan, for example to buy a car, moving costs, or even a getaway, can also be a good way of building a reputation. Making the payments on time every month shows lenders that you can be trusted not to default on a loan. “Defaulting” is the term used to refer to a failure to pay back.

Leasing of appliances, furniture and cars is also included under this.

Unfortunately, even smaller loans can be rejected if you don’t have much of a credit history. Once again, however, it’s not a mark against you if you haven’t had any loans in the last 24 months, it’s just helpful.

- ⭐ Our 24-Factor Credit Check goes beyond your credit score.

- ⭐ See your credit report through a lender’s eyes.

- ⭐ Personalised steps to improve your credit rating.

See… Fix… Borrow… with Credibble.

START FREE TRIALCredit Cards

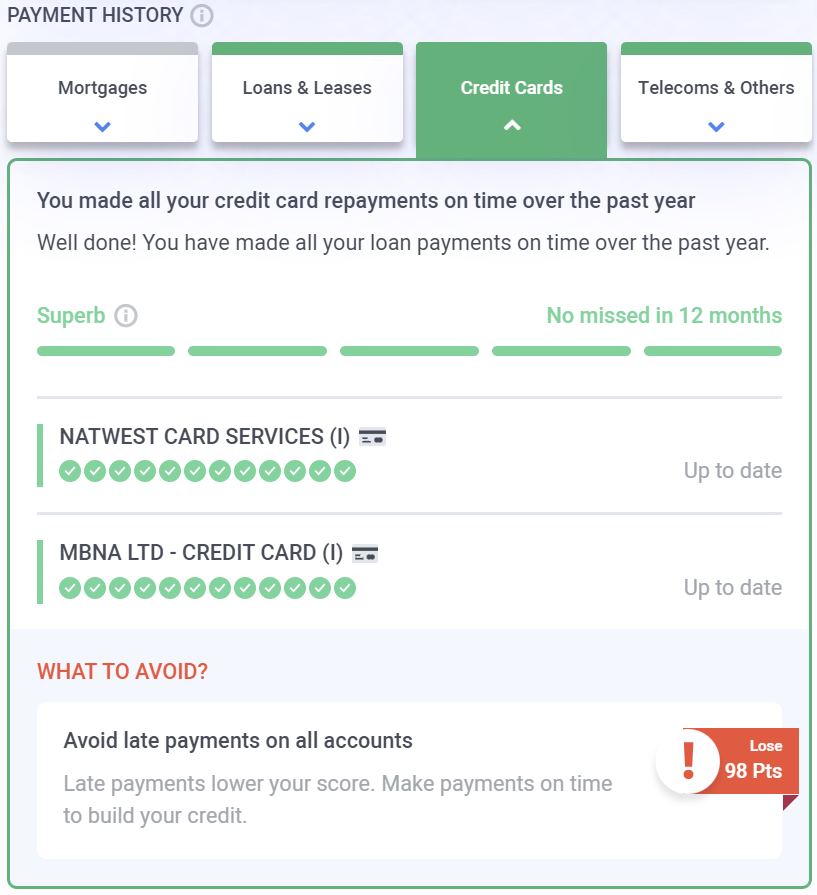

Credit cards are one of the first ports of call for many people looking to build credit. Many organisations today offer “credit builder” cards, usually with lower limits. These give new borrowers a chance to prove themselves.

While they certainly aren’t something you should apply for without careful consideration, they can be a good starting point. Paying off your credit card balance on time each and every month can help give lenders the confidence that their money is safe in your hands.

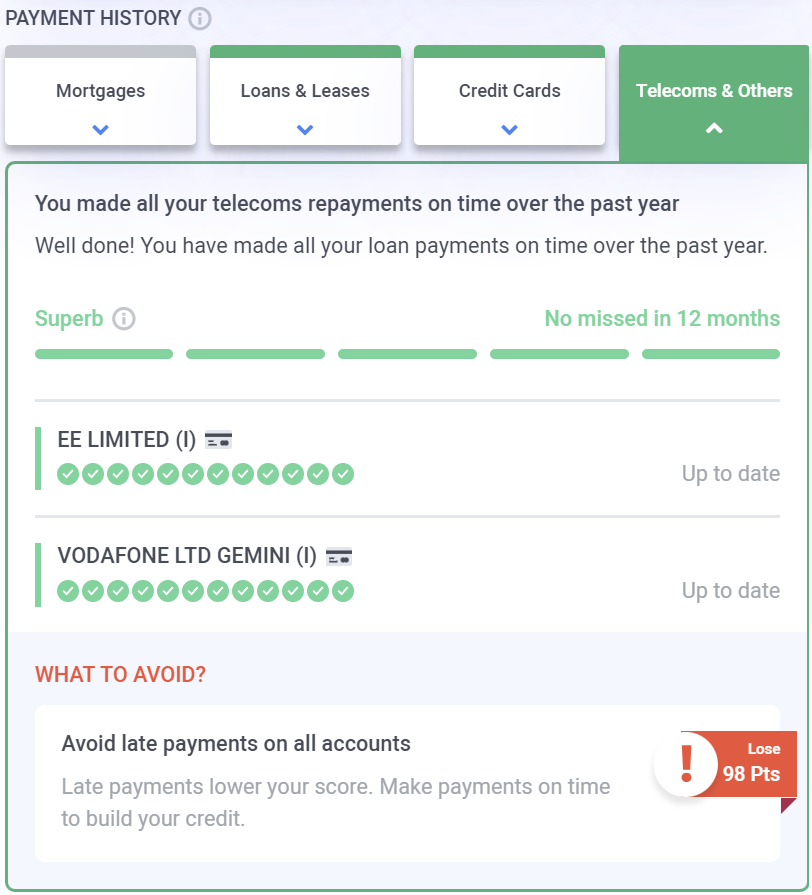

Telecoms & Others

Did you know that many of your bills affect your credit rating? Bills like council tax don’t affect your rating. However, many commercial bills do, including utility bills and telecoms bills (such as Internet). It’s important to try to make bill payments on time every month.

One good way you can start building credit right away is by getting a mobile phone contract. If you’re on a pay-as-you-go SIM, lenders might assume you can’t spare the expense. If that’s true for you, consider making the switch. It’s usually quick and simple, and it can help get you started on your credit journey.

Credibble offers two fabulous solutions

If you’re preparing to take a mortgage, never apply until you’ve tried our unique and FREE Credibble Home app. Our smart technology will tell you what you need to fix so you avoid rejection. The app predicts when you will be able to buy, for how much and tracks your month-by-month progress to mortgage success. We’ve even added your own mortgage broker, so you get the best deals available.

More focused on your credit rating? Well, get started for free with Credibble’s 24- Factor Credit Check to truly help you improve your creditworthiness and how lenders view you. (Remember: lenders don’t use your credit score! We’ll show you what lenders look for and how to get your credit report in the best shape possible).

Last updated by Robert Edwards, May 2022