Sometimes lenders and other firms will run a credit check if you apply for credit or use other services. By reviewing your credit record, they can offer a variety of things, including insurance or credit quotations and allow you to borrow money through loans. Credit check inquiries can be hard or soft – we’ll consider the differences and the impact on your credit rating, if any.

What's Included?

What is a credit check?

A credit check, or credit search, is a process where a company reviews information from your credit report to understand your financial habits better. While they typically require a legitimate reason (such as a loan application), they don’t always need your explicit consent. This check is commonly performed by banks, credit providers, utility suppliers, landlords, mobile phone companies, and employers (although employers won’t see your full report).

Companies may assess your payment history, current credit status, and overall credit management during a credit check. They may also review any financial associations you have, such as shared bank accounts or mortgages, as well as the credit history of those individuals.

It’s important to note that viewing your credit report or score won’t impact your score or affect the likelihood of being approved for credit, no matter how many times you check.

There are two types of credit checks: soft credit checks (or soft searches) and hard credit checks (or hard searches).

- ⭐ Our 24-Factor Credit Check goes beyond your credit score.

- ⭐ See your credit report through a lender’s eyes.

- ⭐ Personalised steps to improve your credit rating.

See… Fix… Borrow… with Credibble.

START FREE TRIALHow Soft Credit Searches Impact Your Credit Report

Soft credit searches are a common practice among credit companies. Unlike a deep credit search (hard search), a soft credit check only requires your basic credit history information. These searches do not affect your credit score or future credit applications. They are visible only to you on your report. Understanding these types of searches can help you make better-informed decisions about your credit. A soft search is also performed when you check your credit score.

How Does a Soft Search Work?

When it’s time to make a purchase requiring a credit check, shopping around is essential. But how do you find the best credit offers for your needs? By using comparison websites that utilise soft credit searches, also known as quotation searches.

A soft credit search is based on your information to determine your eligibility for credit. This can include information used to verify your identity and assess your affordability. For example, obtaining a ‘mortgage in principle’ involves a soft credit cheeck that helps you determine what kind of mortgage you can get from a lender based on your current circumstances. Equally, if you are looking for car finance, you’ll initially have a soft search to see the options available.

You can submit a formal application once you find the right deal, such as a mortgage or credit card offer, the company you apply to will perform a hard credit search, which involves scrutinising your credit history in detail. Remember that even if you’re approved based on the basic information provided for a soft credit search, a credit application may still be unsuccessful following a hard credit search.

In summary, by understanding how a soft credit search works, you can use it to your advantage to find the best credit offers available.

What is a hard credit check?

So, what is a hard search (also known as a hard credit check)? A hard credit check occurs when a company thoroughly investigates your credit report. Each hard check is documented on your credit file, indicating to any entity searching it that you’ve requested credit.

Multiple hard credit checks over a short period can negatively impact your credit score for six months, reducing your ability to secure credit in the future.

When you apply for credit from a company, they will conduct a hard check of your credit report to assess your eligibility. However, utility providers and mobile phone companies may also subject you to a hard check when applying for their services.

How are soft and hard credit checks different?

Are you confused about the difference between soft and hard credit checks? Let’s clear things up. Soft credit checks are conducted without affecting your credit score or being visible to companies. On the other hand, hard credit checks can lower your score and are visible to companies.

Examples of soft credit checks include searching your credit report or using Credibble to compare your credit options. Examples of hard credit checks include applying for a loan, credit card, mortgage, utility service, or pay-monthly mobile phone contract. Knowing the difference can help you make informed decisions about your credit.

Why are soft credit checks useful?

Soft credit checks are a valuable tool for determining your credit eligibility without impacting your credit report. Whether you are seeking a loan for a vacation or a credit card (credit card soft search) for everyday purchases, soft checks allow you to assess your options without actually applying. The best part? You can have as many soft checks as you like, and they have no impact on your credit score, even when done in quick succession.

Can you fail a soft credit check?

Many consumers have asked, “Can I fail a soft credit check?” The answer is no. A soft credit check is not a credit application, so there is no “pass” or “fail” outcome. Instead, it only provides an overview of your credit profile for informational purposes. However, a soft credit check can give you an idea of whether you will likely be approved for credit.

Why Hard Credit Searches Affect Your Credit Score

Are you aware that having numerous credit applications in a short period may lead companies to think you’re in financial trouble or rely too heavily on borrowing? This is because a hard credit check reveals that you’ve applied for credit, implying that you may pose a higher risk to lenders.

Submitting too many credit applications simultaneously can increase your chances of getting denied for credit and may negatively affect your credit score. Our guide on common reasons why individuals are refused credit provides further information.

When do hard searches get removed?

It’s essential to keep in mind that most hard inquiries remain on your credit report for up to 12 months. Read on to learn more about why hard credit checks impact your credit score.

Can I avoid hard credit checks?

Want to avoid hard credit checks? Limit your credit applications! Better still, only apply for credit that you are eligible for. Doing so increases your chances of a favourable credit report and minimises any negative impact.

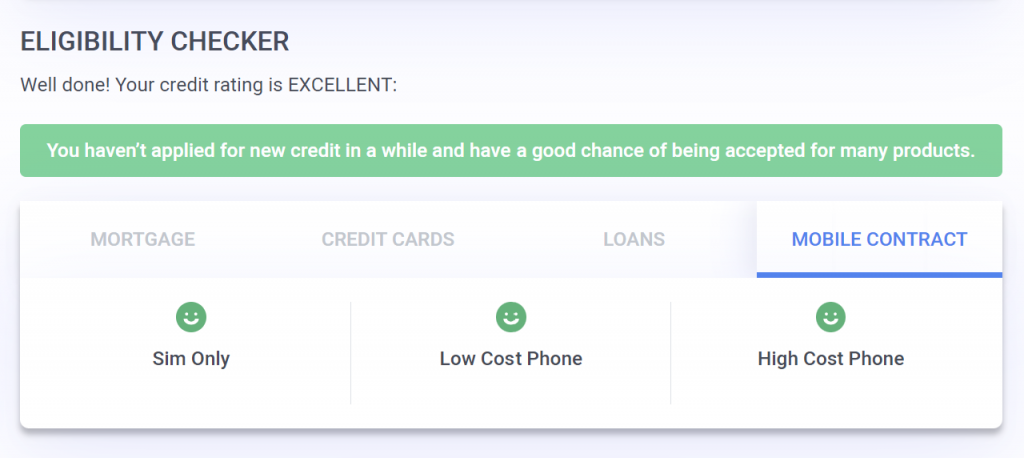

Now here’s a neat trick. Check your eligibility! Credibble’s built-in Eligibility Checker analyses your credit report for everything from credit cards to personal loans, mortgages and mobile phone contracts— all without adversely affecting your score! You receive a soft search, meaning your credit rating won’t be impacted unless you decide to apply. Try it today!

Can I get hard searches removed?

As much as we would like to respond positively, we have to be clear and direct: you cannot remove a hard search if it results from a credit application you made. Nonetheless, after a year, most hard searches will disappear from your credit report.

On a different note, if you find an unfamiliar hard search on your report, this occurrence might indicate fraud or identity theft. Unfortunately, if you fall victim to fraudulent activity, the lender should swiftly address the issues on your credit report and this will adjust your score.

How can you reduce the impact of hard credit checks?

To minimise the negative effects of hard credit checks, consider spreading out your credit applications over a few months. Limiting yourself to two or three applications during this time frame is generally recommended. Keep in mind that each company may have varying criteria for credit scores.

If your credit score does take a hit from a credit application, don’t fret. There are measures you can take to restore and maintain a healthy score.

How to improve my credit score?

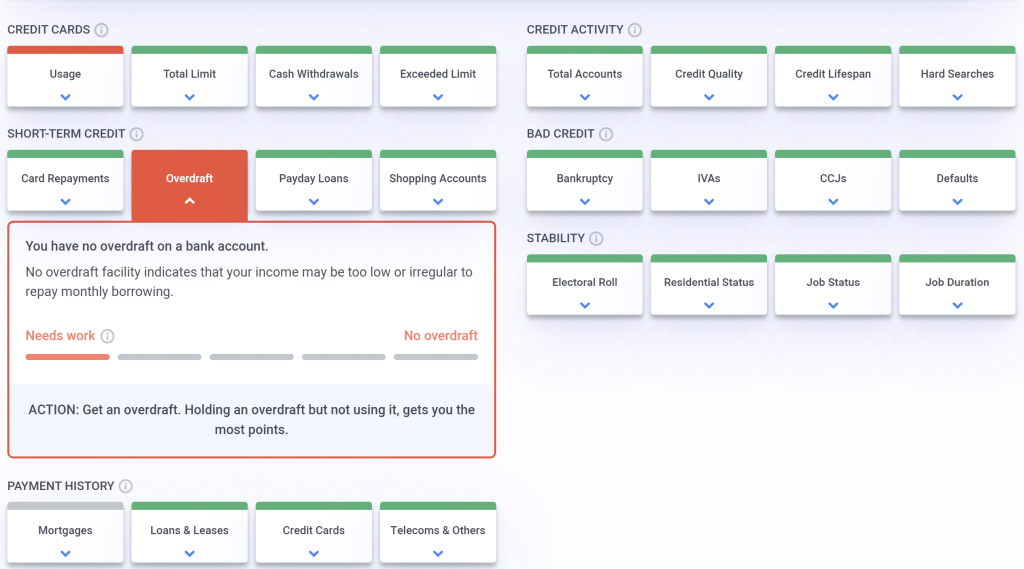

Here at Credibble, we’re helping you take control of your credit score with our innovative soft search 24-Factor Credit Check. Teaming up with the experts at Equifax, our nerdy tech analyses your credit report to give you the most important information – no damage done to your credit rating in the process! Plus, we’re here to flag any red flags on your report and guide you towards fixing them with personalised advice.

With the 24-Factor Credit Check, you’ll get customised action steps based on your report’s changes. So, we’ve got you covered whether you’re in dire straits or looking to cross that credit rating finish line with flying colours. Why not try a 30-day free trial and see the problems your credit score is hiding? You’ll get access to Dual credit and email fraud monitoring, the Credibble Home App for mortgages and your full credit report.

Frequently Asked Questions

How many points does a soft credit check drop your score?

Soft inquiries are not affected by your score. A lender sometimes requests a credit score for your credit file if they conduct a soft investigation.

Can companies see soft credit searches?

Soft searches are also invisible to companies, which will not affect your credit score or future credit requests. All your data is visible in an audit; no one knows the number.

Does a soft credit check show CCJ?

CCJs are visible on a soft search. A soft search is essentially a snapshot of your financial history that encompasses a variety of personal details such as your name, address, and date of birth. It also lists the types of credit you currently have, which can include bank accounts, loans, credit cards, and any outstanding debts.

How long do hard searches stay on credit file uk?

Hard inquiries remain on your credit file for 12 months, after which they naturally disappear. Their impact on your credit rating also fades across the 12 months. However, too many hard searches over a short period can impact your credit rating for up to six months, potentially reducing your eligibility to receive credit during this time.

Does a phone contract eligibility checker run a soft search?

For a contract phone eligibility checker, in almost all cases, the answer is yes. You can have unlimited soft searches on your credit report without impacting your credit score or report. Credibble has a built-in eligibility checker to avoid applying and getting a rejection. If you’re to get a mobile phone with bad credit, you’ll get personalised actions about how to improve your chances.

How long do searches take?

Soft searches usually only take seconds, whereas hard searches delve deeper into your credit file, so can take minutes. As technology improves, these times will likely improve.

How many soft inquiries is too many?

Soft inquiries are not considered when calculating your credit rating, so the number does not matter.

How can I improve my credit score?

Smart ways to improve your credit score and, more importantly, your credit rating include:

- Being prompt and paying all your bills in full

- Keeping a low Credit Card Usage (also known as credit utilisation), which means using a small percentage of your available credit

- Signing up for the Electoral Roll or Register to assist the banks in locating where you live

- Rectifying inaccuracies on your credit report

- Refraining from making too many credit score inquiries in a brief period

References:

How lenders decide whether to give you credit – Citizens Advice https://www.citizensadvice.org.uk/debt-and-money/borrowing-money/how-lenders-decide-whether-to-give-you-credit/