Help to Buy Equity loans are loans which are put towards the cost of buying a home alongside a mortgage and your deposit which allow you to start with only a 5% deposit, allowing prospective buyers to get a foot on the property ladder.

As you take out a smaller mortgage, better mortgage rates are available to you. The loan is not repayable until you either sell the house or 25 years pass, whichever comes first. It’s worth noting that the loan amount is based on the value of the property, so if an independent valuation values the property much higher on sale, or at repayment, you’ll be expected to pay 20% (or 40%) of the value. The amount actually lent to you is not significant.

Equity loans are an affordable homeownership scheme ran by the government where they will give you a loan for up to 40% of the value of a property that you are buying (20% outside of London).

You only need a 5% deposit (of the full purchase price of the property), then you take the rest (75% or 55% in London) as a mortgage.

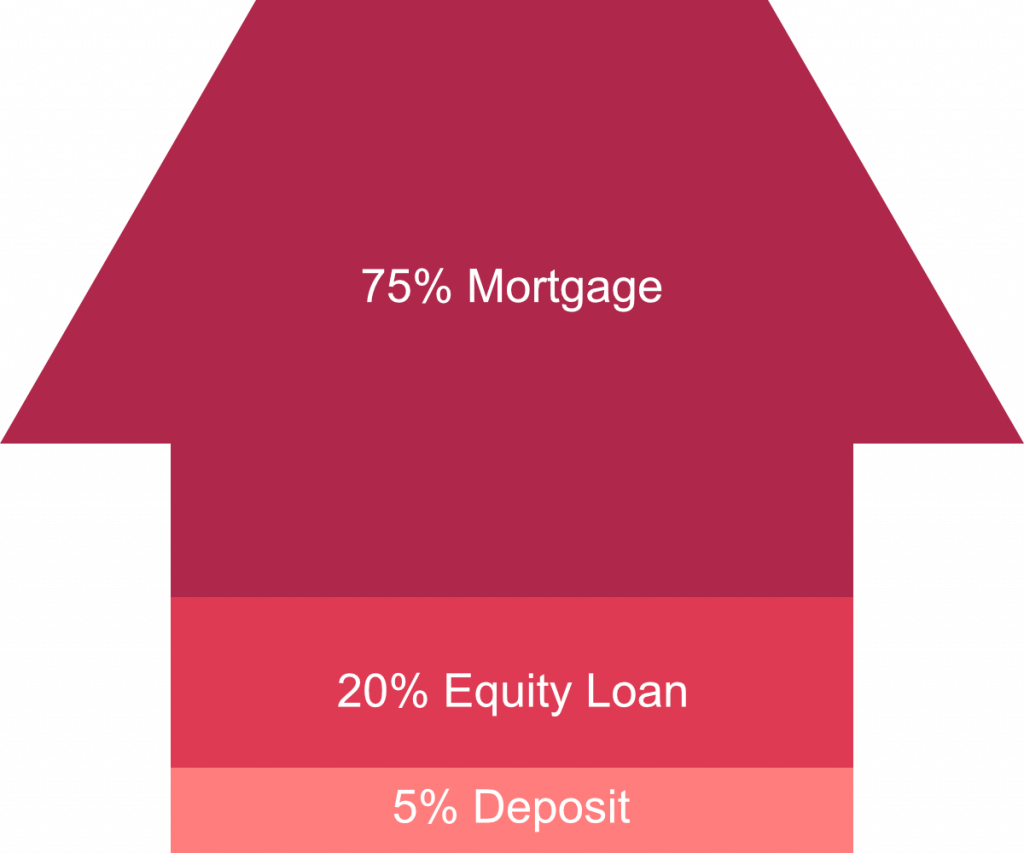

For example, with a house costing £200,000 outside of London, it would be broken down like this:

5% deposit – £10,000

20% Equity loan – £40,000

75% Mortgage – £150,000

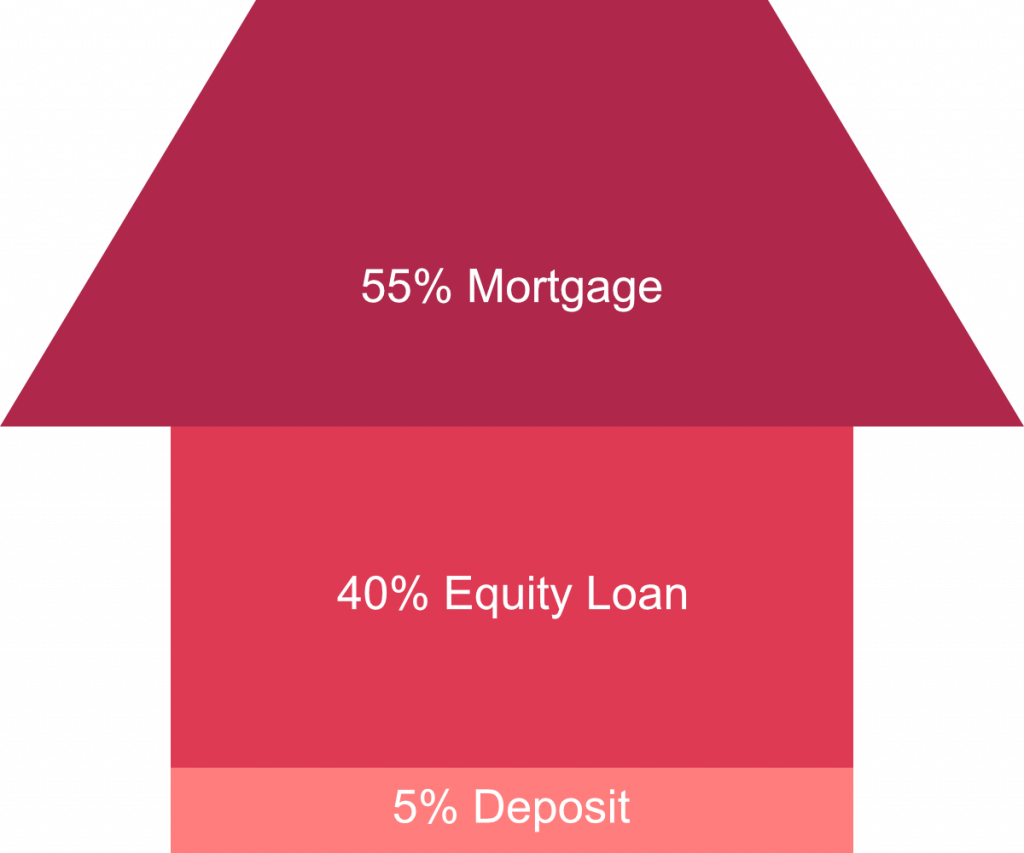

If you had a house costing £200,000 inside London, you could do this:

5% deposit – £10,000

40% Equity loan – £80,000

55% Mortgage – £110,000

What's Included?

Why choose a Help-to-Buy equity loans?

The main reason why you might choose to do this is that your deposit only needs to be 5% of the purchase price. Such a low deposit percentage means that significantly more first-time buyers are able to get on the property ladder.

Alongside this, having up to 40% covered on an equity loan means that you’re taking out a much smaller mortgage, and can, therefore, access better rates.

Eligibility

In order to use the Equity Loans scheme, you must be eligible. The requirements are:

- You must be a first-time buyer or a homeowner that is looking to move.

- You must intend to live in the property that you are buying. This is not available to you if you are planning on letting out the property.

- You cannot use the scheme if you plan to take a mortgage that is more than 4.5 times your household income.

- The property must be a new build at a maximum cost of £600,000.

How do equity loans work?

As with all home purchases, you start by saving up a deposit of at least 5% of the purchase value and spend six to twelve months building up your creditworthiness by completing your booster tips on credibble.com. Browse help to buy properties in the area you wish to buy in to get an idea of how much of a deposit you will need. The home needs to be a new build property that costs no more than £600,000.

Ensure that you have:

- A reservation fee (maximum of £500)

- Your deposit amount – at least 5% of the purchase amount

- The funds for other fees, such as stamp duty, legal fees, removal fees, and survey fees.

When you think you’re ready to buy, you can use websites such as Homes for Londoners and Help to Buy to find homes and help to buy agents in the area that you want to buy-in. After choosing your home, you fill out some paperwork and put a reservation fee on the home.

Once you’ve had the go-ahead from your local help to buy agent, you’ll be able to apply for a mortgage. Your mortgage must be at least 25% of the purchase price of the property and your mortgage and cash deposit must cover at least 80% of the property price when added together. Meanwhile, your solicitor or conveyancer will go through the process of the equity loan with you. The equity loan can cover up to 20% of the purchase price, or 40% if the home is in London.

Once completed, your mortgage lender will provide its funds, and Homes England will provide theirs – you’ll own the home and can officially move in.

Repaying the Equity Loan

From taking out the loan, you’ll need to pay a monthly management fee of £1. This is payable until the loan has been fully repaid. 5 years after you purchase the property, you’ll need to start paying an additional fee in the form of interest. This will be 1.75% and will go up annually. This will be payable until the loan has been repaid.

If you sell your home before 25 years then you must repay the equity loan – this is the same percentage of the proceeds of the sale, so if you sell the house for more than it cost when you bought it, the value of the 20% covered by the loan has gone up and the repayment must reflect this. If the house sells for less than you bought it for then the amount that you repay will be less than you originally borrowed. This must be approved by Homes England prior to the sale.

If, after 25 years, you are still living in the property you purchased with an equity loan then it must be repaid.

Staircasing

You are able to repay all or part of the equity loan to Homes England. If you make a partial payment, then it is known as staircasing.

You can make a staircasing payment at any time, but it must be a minimum of 10% of the home’s market value. An independent valuation of the property must be made in order to do this, the costs of which are payable by you.

You can extend your mortgage to make a partial payment on your equity loan. As a result, your mortgage payments will increase. Homes England need to approve this.

The interest fees that you pay on the equity loan after 5 years will reduce as a result of a part payment to reflect the change in the total that you are borrowing.

Maintenance

As with shared ownership, you will be liable to pay for any maintenance or repairs to the property. New build homes tend to have a guarantee of up to 10 years which will cover any defects due to the workmanship.

You’ll need permission from Homes England to extend or make any alterations to the property. It’s recommended that you repay your equity loan prior to making any alteration plans.

If modifications need to be made to make the property more accessible in the case of disability, Homes England will act reasonably and are more likely to consider granting you consent to make the changes.

If you want to read about any other affordable homeownership schemes then you could consider the Help to Buy ISA or Shared Ownership, click on the corresponding name to read an article on each of these to see if they are suitable for you.

Credibble offers two fabulous solutions

If you’re preparing to take a mortgage, never apply until you’ve tried our unique and FREE Credibble Home app. Our smart technology will tell you what you need to fix so you avoid rejection. The app predicts when you will be able to buy, for how much and tracks your month-by-month progress to mortgage success. We’ve even added your own mortgage broker, so you get the best deals available.

More focused on your credit rating? Well, get started for free with Credibble’s 24- Factor Credit Check to truly help you improve your creditworthiness and how lenders view you. (Remember: lenders don’t use your credit score! We’ll show you what lenders look for and how to get your credit report in the best shape possible).

Last Updated by Oliver Macmillan, May 2022